Since 2016, the continuous fermentation of supply-side reforms in the steel industry has become a major weapon in the rise of steel stock prices in the past two years. For the steel industry with obvious cyclicality, the iron and steel “four gold and silver four†claims have been in existence for a long time. The annual start-up season of March-April can bring certain demand growth to steel enterprises, which in turn makes steel enterprises basically The face gets a relatively good promotion period. Nowadays, supply-side reform is still the main theme of the industry in 2018, and the demand for the peak season is likely to surpass the previous year's background. There is still momentum in the upward trend of steel prices, which makes the basic expectations of steel stocks continue.

The start of the construction season, the impact of negative disturbance factors is limited

Since the beginning of this year, the overall performance of steel stocks has been flattened compared with the sustained sharp increase in the previous two years. The performance of individual stocks has also begun to diversify. Especially since March, the steel sector has fallen by 3.78 compared with the previous two months. %, the so-called "Golden Three" market does not seem to have a good start.

Regarding the unfavorable opening of the “Golden Three†market, market participants believe that in addition to the cumulative increase of more than 8% in the first two months of this year, which has led to adjustments, the United States intends to impose a 25% tariff on imported steel and a post-holiday steel society. Factors such as high inventory levels have also had a certain inhibitory effect on the rise in steel prices, which has led to an increase in negative market sentiment.

"The direct impact of US tariffs on imported steel on China is limited." Liu Zhe, president of Wanbo Brothers Asset Management Co., Ltd. and vice president of Wanbo New Economic Research Institute, believes that Chinese steel enterprises have relatively limited steel exports to the United States. According to the data, China's steel exports accounted for only 7.19% of China's steel output in 2017. The highest rankings of steel imports from China in 2017 were South Korea, Vietnam and the Philippines. The United States ranked only 26, and China's exports to the United States were 118. Ten thousand tons, accounting for 1.56% of China's steel exports, accounting for 0.11% of China's steel output (see Figure 1).

"The US steel tariffs aimed at lifting is not a Chinese, worrying or other countries began to follow suit once the United States, would cause huge blow to the global steel industry chain." Shanxi Securities 002500, shares strategist attending Ma Wen Yu believes that the impact of domestic steel companies on the proposed tariff increase on imported steel in the United States is relatively limited. She also believes that from the perspective of current global trade, the possibility of other countries emulating the United States is still relatively low.

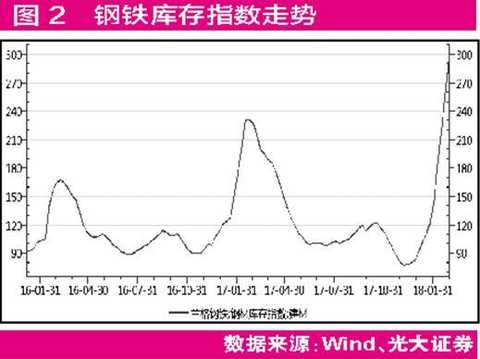

For steel companies, the most noteworthy issue is the steel inventory problem. At present, the problem of how to digest the high social stocks of five major steels, such as rebar and hot rolled coil, has become a major uncertainty in the follow-up steel price trend (see Figure 2). However, industry insiders believe that this is because the actual demand has not yet started. As the weather in March has gradually warmed up, the arrival of the peak season is expected to lead to a gradual recovery of the downstream industry of steel, and the recovery of demand will lead to the gradual entry of goods into the market.

In the steel demand side, investment in long-term infrastructure investment, although the investment scale of railway fixed assets plan in 2018 decreased by 68 billion yuan from 2017, down 8.5%, the investment scale of highway waterway transportation plan was flat, and the scale of water conservancy projects under construction reached 10,000. 100 million yuan, an increase of 11%, but from the actual completion of the past year, such as 2017, the actual investment in railways in 2017 is basically the same as planned investment, and the actual investment in highways exceeds the planned 26%. On this basis, although the planned investment amount in 2018 has decreased compared with the actual investment amount in the previous two years, the industry expects to maintain a high level (see Table 1).

The property sector, Sealand Securities 000750, diagnosis equity strategists believe Daipeng Ju, due to policy control, real estate sales growth pressure but certainly able to maintain growth above 10%, interest rates up slowly, housing prices will to start re-stocking is strong, The growth rate of real estate construction is expected to be between 6% and 7%. In the downstream manufacturing of sheet metal, the recovery of engineering machinery, petroleum and petrochemical industries is good, and the demand for steel in automotive and other industries will remain high.

Environmental protection stacks to capacity, supply contraction logic strengthens

2018 is the first year that the country has determined to be the top three battles for environmental protection. As one of the heavily polluting industries, the steel industry is expected to be stronger than last year.

On February 23, Tangshan City, Hebei Province, a major steel producing province, issued the “Tangshan Iron and Steel Industry 2018 Non-Heating Season Peak Production Plan†(draft for comments), stipulating that non-heating season steel enterprises will carry out peak production, and the impact is expected. The blast furnace ironmaking capacity is 9.875 million tons. At the same time, 邯郸 also released two steel industry limited production documents, respectively, in March, the city's 18 steel companies are strictly limited production capacity of 50% (in the blast furnace), in the second and third quarter, there is "not reaching the ultra-low emission limit" Steel companies that are one of the top five problems limit production by 20%. The market generally believes that the Tangshan and Chongqing limited production programs show a trend of normalization in the non-heating season. The introduction of the new policy of restricting production in the two places is the first shot that has started the environmental protection of the steel industry this year.

Founder Securities 601901, attending stocks analyst Wang Xiwen think, Tangshan and Handan limited production release of the New Deal will be the country's increasingly demanding environmental protection industry a start, the follow-up does not exclude other areas has started to be normalized to limit production, environmental protection and supply of steel industry The impact of the suppression will be throughout the year, and the limit of production is expected to exceed market expectations. In fact, Hebei Province clearly stated on March 8 that this year it will reduce steel production capacity and iron production capacity by more than 10 million tons each. This is compared with the previous report of the Hebei Provincial Government Work Report that “the annual production capacity of steel is reduced by more than 10 million tons. The plan has doubled.

In addition to shrinking supply due to environmentally limited production factors, supply-side de-capacity will also strengthen supply-contraction logic. In the past two years, steel production capacity has reached 65 million tons and 50 million tons respectively. In 2018, it will “repress and reduce steel production capacity by 30 million tonsâ€. In terms of the decision on the target of steel production capacity, Liu Zhe told the reporters of "Red Weekly" that "the goal of steel production capacity reduction in 2018 is significantly reduced, and the marginal impact of the total supply contraction will decline. In the future, zombie enterprises, backward production capacity, The environmentally-friendly non-compliance capacity is a breakthrough, and the focus of the supply-side structural reform of the steel industry will shift from total control to structural adjustment and optimization."

Similarly, the impact on steel production capacity, Ma Wenyu believes that "as the supply side reform is coming to an end, the production base is shrinking, the effect of de-capacity will show a marginal rise, the reason is that with the de-capacity In-depth, capacity utilization is rapidly rising, and the problem of oversupply will be completely reversed. This means that although the amount of capacity going on this year has declined, the effect will not be much worse than 2017." According to further analysis, in the case of completing the capacity-removal target in 2018, the utilization rate of coal and steel capacity has exceeded 80%, which should be calculated by the management. Because according to international standards, 80% capacity utilization means a basic balance between supply and demand. This means that the problem of oversupply in the steel and coal industries has basically been reversed.

The performance improvement valuation is obviously repaired

It is precisely in the past two years that supply-side reforms have continued to advance, and the performance of listed steel companies in 2017 is also very eye-catching. According to statistics, a total of 33 A shares from iron and steel enterprises in 2017 annual results notice, and official results Letters earnings point of view, with the exception Xining Special Steel 600 117, without any consultation shares temporarily annual data, other steel companies have disclosed the relevant annual reports content. It is noteworthy that, provided the annual performance of the company 32 cases, only Fushun Special Steel 600399, attending pre-hi stock performance, the other 31 all to the good performance of the company.

From the perspective of forecasting the lower growth margin of net profit year-on-year (overlapped with the official earnings report company), Bayi Iron & Steel Co., Ltd. 600581, Diagnostic Stock , Songshan Songshan, 00017, Diagnostic Stock , Baotou Steel 600010, Diagnostic Stock , Anyang Iron and Steel 600569, clinic shares, Liuzhou Iron and steel shares 601003, shares of five companies attending expects 2017 net profit will achieve double the growth of these common environmental characteristics, supply-side reforms to be able to affect the production of the main business generated a high growth companies (see Table 2 ).

Taking Anyang Iron and Steel as an example, in 2017, the company expects to achieve a net profit of 1.55 billion yuan to 1.75 billion yuan, a year-on-year increase of 1158% to 1320%. The company said that in 2017, it benefited from a supply-side structural reform, defusing excess steel production capacity, and completely banned a series of policy measures such as “strip steelâ€. The steel supply and demand structure was continuously optimized, steel prices returned reasonably, and the steel industry as a whole Business is improving, and corporate profits have also grown steadily.

In addition to the general improvement in industry performance and the doubling of net profit of individual companies, some steel companies have successfully achieved “uncapâ€. For example, on March 8, *ST Chongqing Iron & Steel announced that in 2017, the company achieved operating income of 13.237 billion yuan, a year-on-year increase of 199.82%, of which the main business income was 13.211 billion yuan, an increase of 201.00%. The company achieved a net profit of RMB 320 million attributable to shareholders of the listed company throughout the year, and realized a turnaround to profit. On the second day after the announcement (March 9), *ST Chongqing Iron and Steel Co., Ltd. cancelled the delisting risk warning, and subsequently Changed its name to Chongqing Iron and Steel 601005, the stock . Similarly, *ST Hualing was also able to "uncap" due to the performance reversal, and changed its name to Valin Steel 000932, a stock .

For the current fundamentals to continue to improve the steel sector, Ma Wenyu told reporters that the supply side reform efforts are not reduced, the environmental protection cooperation capacity shows the multiplication effect, industry concentration increase, thickening profits, performance improvement and the emergence of utility attributes They can be annotated. At the same time, in terms of investment, valuation is also an indicator that needs to be focused on. She believes that “the current valuation of the steel industry is at a historically low level. Once the performance stability is recognized by the market, there is huge room for valuation restoration.â€

The reporter of "Red Weekly" found that the current price-earnings ratio of the steel sector is about 15 times. The valuation is only higher than the banking, real estate and building decoration industries in the 28 first-tier industries of Shenwan. The continuous growth of the performance makes the steel sector's current overall estimate. The value is much better than the 22.8 times at the end of the third quarter of 2017. At the same time, as of the end of the third quarter of 2017, the average return on net assets of the steel industry also increased significantly, reaching 9.24%, ranking sixth in the Shenwan industry. In this regard, Guohai Securities said that from the perspective of fundamentals and valuation, the steel industry will continue to maintain a relatively tight supply and continue to maintain a relatively high level of steel prices in 2018, after de-capacity continues and demand growth is flat. The high profitability of the company is still sustainable.

"In the context of the sharp contraction of supply caused by administrative forces, steel prices have risen sharply in the short term, and the profits of steel companies have rebounded significantly. Performance restoration is the focus of investment in the early steel sector." Liu Zhe said. However, she also pointed out that the price surge caused by supply contraction is obviously unsustainable. Under the premise that downstream demand has not recovered significantly, the price fluctuations of commodities such as steel and coal will gradually return to the demand side, and the investment logic of the steel sector will be It will also change from supply contraction to demand side. “The valuation of the steel industry in the future still needs to consider its cyclical attributes, not just short-term performance, but neglect long-term fluctuationsâ€.

Mens Pu Jacket,Men Winter Pu Leather Jacket,Hooded Men'S Pu Jackets,Men Baseball Pu Jackets

Shaoxing Moonten Trade Co., Ltd , https://www.moontenshirts.com